FORT LAUDERDALE – Is your son or daughter, college-bound? If you have a son or daughter with aspirations to attend college, don’t make the mistake of waiting until they are 18 years of age to start saving for their higher education. With annual costs of more than $45,000 per a year for the average private four-year college, you should seriously consider a 529 College Savings Program with no age restrictions and no income phaseout limits to shield your assets from gift and estate tax. If you’re on fixed income like many residents in Florida, you could drive for Lyft and give your grandchild a gift that keeps on giving with a 529 College Savings Plan.

FORT LAUDERDALE – Is your son or daughter, college-bound? If you have a son or daughter with aspirations to attend college, don’t make the mistake of waiting until they are 18 years of age to start saving for their higher education. With annual costs of more than $45,000 per a year for the average private four-year college, you should seriously consider a 529 College Savings Program with no age restrictions and no income phaseout limits to shield your assets from gift and estate tax. If you’re on fixed income like many residents in Florida, you could drive for Lyft and give your grandchild a gift that keeps on giving with a 529 College Savings Plan.

The “529” as it is commonly referred to comes in two options: (1) State Operated Prepaid Tuition Plan and (2) Saving plan where funds accumulate tax deferred. You could suffer if you wait too long to use the 529 investment vehicles because your state’s 529 Prepaid Tuition Plan is designed to lock in today’s rates at state universities and the state government invests your contributions to cover the future college tuition at sponsoring state eligible colleges and universities. The 529 Prepaid Tuition Plans is great for purchasing units of future tuition where state governments guarantee the cost of education regardless of investment performance or rate of tuition increases.

Why not drive for Lyft and fund your kid’s 529 College Savings Plan. It is just like an investment account, but your funds accumulate tax deferred. As long as your 529 plans are used for qualified college expenses, your 529 college savings plan is free of federal income tax and it can be used for all qualified higher-education expenses. Like any investment vehicle, depending on when your grandchild’s anticipated college entry and the funds required, you can place your investment dollars in a mix of investment funds for desired volatility and performance depending on how close your desired withdrawal dates and college entrance draws near.

Why not drive for Lyft and fund your kid’s 529 College Savings Plan. It is just like an investment account, but your funds accumulate tax deferred. As long as your 529 plans are used for qualified college expenses, your 529 college savings plan is free of federal income tax and it can be used for all qualified higher-education expenses. Like any investment vehicle, depending on when your grandchild’s anticipated college entry and the funds required, you can place your investment dollars in a mix of investment funds for desired volatility and performance depending on how close your desired withdrawal dates and college entrance draws near.

Your 529 contributions are considered to be gifts to the beneficiary so what better way to shield inheritance money from gift tax and estate tax than contributing up to $14,000 per year (2017) in one lump sum or installments. Best of all, 529 assets are held outside the account owner’s estate to avoid estate taxes upon death.

With the rising number of retirees hitting the road with Lyft, what better way to give an inheritance gift to your grandchild than investing your Lyft earnings in a 529 plan with them as the “beneficiary”. It’s the gift that keeps on giving! Your gift grows tax-deferred and free of federal income tax and stays separate from your estate. As you drive for Lyft — you stay motivated with each ride because you’ll get to meet some nice people, earn generous tax deductions and also shield inheritance money from gift and estate taxes. You, as the account owner retains control of the assets and the power to control withdrawals from the account, plus annual gift tax exclusion can be accelerated up to five years by making up to a $70,000 contribution (couples up to $140,000) in 2017 as long as no other contributions are made for five years for the designated beneficiary.

With the rising number of retirees hitting the road with Lyft, what better way to give an inheritance gift to your grandchild than investing your Lyft earnings in a 529 plan with them as the “beneficiary”. It’s the gift that keeps on giving! Your gift grows tax-deferred and free of federal income tax and stays separate from your estate. As you drive for Lyft — you stay motivated with each ride because you’ll get to meet some nice people, earn generous tax deductions and also shield inheritance money from gift and estate taxes. You, as the account owner retains control of the assets and the power to control withdrawals from the account, plus annual gift tax exclusion can be accelerated up to five years by making up to a $70,000 contribution (couples up to $140,000) in 2017 as long as no other contributions are made for five years for the designated beneficiary.

If you’re on fixed income and looking for a great way to bring in an extra $250 – $300 a month, why not give a gift to your grandchild by starting a 529 College Savings Plan and by investing your Lyft earnings whole or in part and enjoy tax-deferred benefits, gift tax and estate tax exclusions. What better way to invest in the future wealth of your grandchild while protecting them from the crippling effects of Federal Student Loan Debt.

Scholarships and grants are another way to protect your grandchild from the burden of Federal Student Loan Debt. With the rising costs of tuition and today’s college graduate entering the workforce with an average debt of $26,000 in student loans, a combination of the 529 College Prepaid Plan and Saving Plan along with scholarships and grants can significantly increase the wealth accumulation of the college graduate by minimizing exposure to the compounding interest of student loan debt.

Do yourself a favor and download Job Ninja’s exclusive “Top 500 Scholarships List” when you subscribe today and take advantage of this powerful information. You will gain INSTANT ACCESS to our exclusive list with URL hop-links for quick reference to over $2.9 billion in free college scholarships and grants. Even if you are enrolled in college, it is never too late to explore all options for earning scholarships and grants to cover eligible college expenses. A 529 College Savings Plan is perfect for making up any difference in qualified higher-education expenses not covered by the scholarship.

(c) FloridaPrepaidPlan.com. “Click & Zoom”.

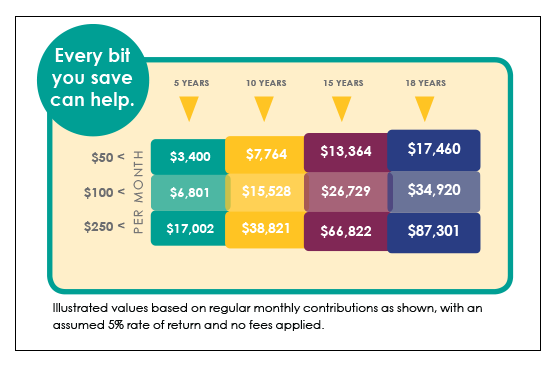

So what is your college savings goal — $20,000, $40,000 or perhaps $80,000? The longer you wait, the more money you will need to reach your savings goal. If you start a 529 College Savings Plan now, it will increase the possibility of earnings shielded from gift, estate and federal income tax. It can all start with signing up for Lyft and investing whole or in part, your Lyft earnings to catch the momentum of compounding interest on your savings.

If you delay your investment, then you are subject to the “flip-side of the coin” – you may succumb to the debilitating effects of student loan compounding interest. Start saving now and let interest compound in your favor. It’s never too late to start saving for college and reaping the benefits of a 529 College Savings Plan!

Take the first step towards giving a great gift to your son, daughter or grandchild and sign up to drive for Lyft. You can drive for 10 hours a week and pocket an extra $$250 – $300 to invest directly into your 529 College Savings Plan for your “beneficiary” and save on gift and estate taxes and watch your earnings grow tax-deferred. The 529 College Savings Plan is a powerful way to “gift” your children and grandchildren a college education while saving on gift and estate taxes. Give the gift that keeps on giving: a college education gives children options in Life – where they live, where they get to send their children to school and the freedom to witness and embrace the beauty of this World we call Home.

*There are fees associated with almost every investment vehicle so discuss your options with your legal/tax adviser as objectives, risks and volatility must be reviewed and considered carefully before investing.

Reference: Dr. Martin Luther King, Jr., “Where Do We Go from Here: Chaos or Community? (King Legacy)”.

Reference: Steve Jobs, “Steve Jobs”.